PV function in Excel, your financial ally, simplifies complex calculations, allowing you to determine the present value of future cash flows effortlessly. Whether you’re assessing investment opportunities, evaluating loan terms, or planning for retirement, PV function is your financial compass. With precision and efficiency, it helps you make informed decisions by putting the current worth of future cash flows at your fingertips. Excel’s PV function is a versatile tool that empowers financial analysts, investors, and planners to navigate the intricacies of finance with confidence. Start using PV function in Excel today to unravel the value of your financial decisions and secure a brighter financial future.

These content covers:

- What does PV Function mean?

- Syntax, Arguments.

- 5 PV function basics that you should be aware of?

- Excel formulas that demonstrate how to use the PV function.

- Calculate PV of annuity.

- Determine the investment’s PV based on its future value.

- Excel formulas for NPV and PV differ from one another.

1. What does PV Function mean

PV is an Excel financial function that returns the present value of an annuity, loan or investment based on a constant interest rate. It can be used for a series of periodic cash flows. If someone wants to know the present value of future cash flows then they can use that function. You will be known the further information about present value by below part.

2. Syntax, Arguments

=PV(rate, nper, pmt, [fv], [type]) where:

- Rate(required arguments) – the interest rate per period. If you make yearly payments, indicate an annual interest rate; if you pay monthly, specify a monthly interest rate, and so on.

- Nper(required arguments) – the total number of payment periods for the length of an annuity.

- Pmt(required arguments) – the amount paid each period. If omitted, it is assumed to be 0, and the fv argument must be included.

- Fv(optional arguments) – the future value of an annuity after the last payment. If omitted, it is assumed to be 0, and the pmt argument must be included.

- Type(optional arguments) – when the payments are to be made.

- at the end of a period (regular annuity) and 1 – at the beginning of a period (annuity due).

3. 5 PV function basics that you should be aware of.

Please remember the following usage guidelines to ensure that your worksheets’ use of the Excel PV function is successful:

- The pmt argument must be present and vice versa if the fv argument is 0 or absent.

- The rate argument can be given as a decimal or percentage, for example, 10% or 0.1.

- A negative figure should be used to reflect any money you spend (outflow). A positive integer should be used to reflect any money you receive (inflow).

- When calculating periodic cash flows, be consistent with the rate and nper units. For instance, if you make 5 yearly payments at a 7% annual interest rate, use 5 for nper and 7% or 0.07 for rate. If you make monthly payments for a period of 5 years, then use 5*12 (a total of 60 periods) for nper and 7%/12 for rate.

- All the arguments must be numeric, otherwise the PV function returns a #VALUE! error.

4. Excel formulas that demonstrate how to use the PV function

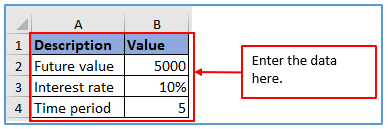

For measure the present value you can follow this formula: = future value/(1+interest rate)^period. Here is an example of PV, Suppose you want to get 5000 after 5 years with 10% interest rate. so how much do you want to deposit right now?

Step 1: Enter the above information into the Excel.

Placed the data below.

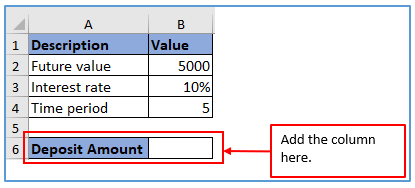

Step 2: Add the columns in A6 and B6 to get the deposit amount.

The column has been added.

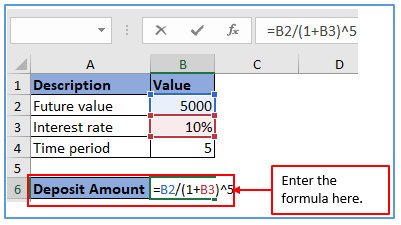

Step 3: Now, enter the formula: =B2/(1+B3)^5

The formula is used here.

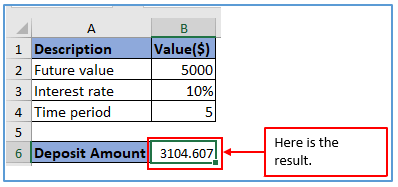

Step 4: Press the enter and get the result.

Here is the result.

5. Calculate PV of annuity

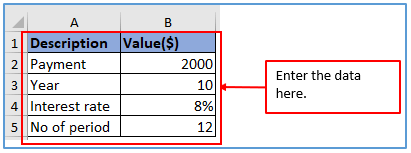

Here is an example: Suppose, a regular payment of $2000 is to be made to the insurance company at the end of every month for the next 10 years. The annuity earns an 8% annual interest compounded monthly. The question is – how much is this annuity worth now?

Step 1: Input all the above information into the excel as shown below.

Here is entered all the data below.

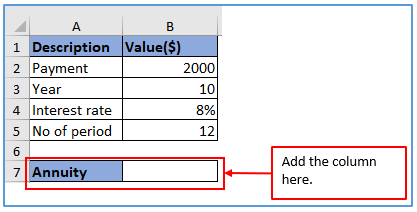

Step 2: Add the columns in A7 and B7 to get the result of annuity.

The column has been added.

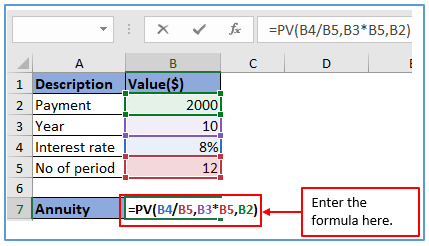

Step 3: Now, use the formula: =PV(B4/B5,B3*B5,B2)

The formula is used here.

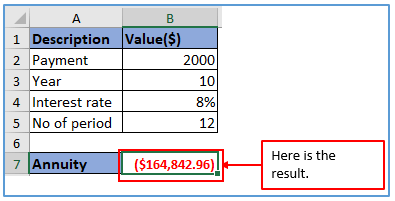

Step 4: Press the enter and get the value.

The result is below here.

6. Determine the investment’s PV based on its future value.

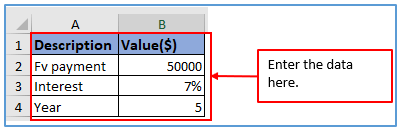

Here is the example of PV based on its future value: In this example, we are going to find the present value of an investment that will pay $500,000 in 5 years, with an annual interest rate of 7%. How much money do you need to invest today to reach the target amount at the end of the investment period?

Step 1: Enter the above information into the Excel.

Placed the data below.

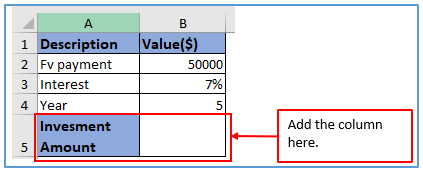

Step 2: Add the columns in A5 and B5 to get the result of annuity.

The column has been added.

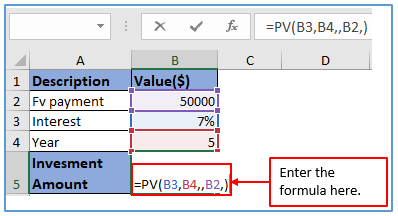

Step 3: Now, use the formula: =PV(D5,D6,,D4,). Here use a double comma to skip the formula value. Here there is no PMT and that’s why you need to use double comma.

The formula is used here.

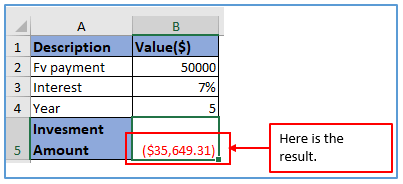

Step 4: Press the enter button to get the future value.

The result is outlined below .

7. Excel formulas for NPV and PV differ from one another.

In addition to PV, there is another term in finance called NPV that estimates the current value of future cash flows by discounting them by an anticipated rate of return. Although these two names share many characteristics, they also differ significantly.

-Future cash inflows for a specific time period are referred to as “present value” (PV).

-The difference between the current value of cash inflows and outflows is known as net present value (NPV). In other words, the present value is a net amount because NPV accounts for the initial investment.

The two key distinctions between the PV and NPV functions in Microsoft Excel are as follows:

-Only steady cash flows that don’t alter over the course of an annuity’s lifetime can be calculated using the PV function. Variable cash flows can be computed using the NPV function.

-PV is effective for both annuities due and ordinary annuities. Only cash flows that happen at the conclusion of each period can be handled by NPV.

Application of PV function in Excel to calculate the Present Value

- Investment Valuation: PV function helps determine the current value of an investment by discounting expected future cash flows, assisting investors in assessing its profitability.

- Loan Amortization: It aids in calculating the present value of future loan payments, helping borrowers understand their financial obligations and plan for repayments.

- Retirement Planning: PV function can be used to estimate the present value of future retirement savings or pension funds, helping individuals plan for a financially secure retirement.

- Business Decision-making: Businesses use PV function to evaluate the profitability of potential projects or investments by comparing the present value of costs and revenues.

- Real Estate Analysis: Real estate professionals utilize PV function to assess the value of rental income or property investments, assisting in informed buying or selling decisions.

- Discounted Cash Flow (DCF) Analysis: In finance and valuation, DCF analysis relies on the PV function to determine the present value of expected cash flows, enabling better investment choices.

In all these scenarios, the PV function in Excel simplifies complex financial calculations and provides insights into the current value of future cash flows, aiding in effective decision-making.

For ready-to-use Dashboard Templates: